INTERESTING STATISTICS

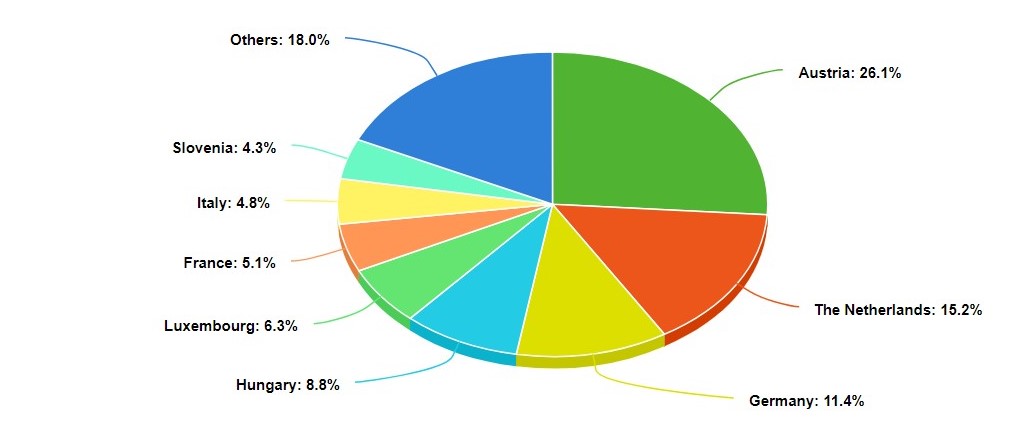

Statistics from the Croatian economy ministry tell us that between 1993 and 2012 foreigners (legal and physical persons) have invested 26.75 billion € in Croatian economy. In the model below, you can see over the years which countries have invested most in Croatia

The rights and duties of foreign investors in Croatia are the same as domestic investors. Foreign investors have the right to claim the income of their companies in their countries of origin. With regard to the acquisition of real estate in Croatia, it evokes the form that both natural and legal persons from EU Member States acquire the right to own property on the basis of the presumptions applicable to the acquisition of the right of ownership for citizens. of the Republic of Croatia and legal entities with registered office in the Republic of Croatia, with the exception of real estate or agricultural land with special law applications as well as for those natural areas with special legislative protection. A foreign investor can, through his company in Croatia, as a national legal entity, acquire real estate without restrictions.

TAXATION

In the Croatian tax system there are a number of measures to stimulate investment, these incentives are defined by different laws. Over the years, from the independence until today, the fiscal system is being modernized in order to favor the development of the country a competitive system of direct foreign investments. The tax treatment for residents and non-residents is equated, while for what concerns the taxation of non-residents and double taxation agreements there is an agreement signed by Croatia with 43 countries, including Italy.

| TAX | PERCENTAGE |

|---|---|

| Legal income tax | 18% |

| Personal income tax (depends on type) | 12% to 40% |

| Surtax (depends on the area of residence) | 0% to 18% |

| VAT (Varies depending on case) | 5% (tourism and primary products) to 25% (trade production and services) |

| Property tax | 4% |

INVESTMENT INCENTIVE IN THE REPUBLIC OF CROATIA

Croatia has opened a program to encourage investment in values determined according to the Investment Act (Zakon or poticanju i ulaganja). Depending on the size of the companies, there are different incentives. For companies called "micro", the vlaori are defined in article 8 of the law. In point 1, with invests of at least € 50,000 and with 3 new jobs, the income tax decreases by 50%, for at least 5 years. As regards the other corporate categories, in article 9 of the law, in the first 3 points there are the definitions of the values that can be used in the next 10 years. In point 1, it is defined that; up to an investment of € 1,000,000 and with at least 5 new jobs, the income tax is paid at 50% of its value, while in point 2, it is defined that from € 1,000,000 to € 3,000,000 and with at least 10 new jobs, the value of the tax decreases by 75%, while at point 3, the value is zeroed with a growth of over € 3,000,000 and with at least 15 new jobs. There are also incentives for the recruitment of new jobs, such as the recruitment of persons defined by law "young" and without having any jobs, that until the age of 30 the company that hires him does not have to pay the contribution for the first year of work. In addition to this, also for the Investment Act, from Article 10 to Article 15, a series of activities are defined to have "stimuli" concerning: recruitment of new jobs, improvements in the field of their activities and other investments private individuals who go to lower taxes to be paid to the state. Obviously to have these incentives, we need to make a series of requests to the agencies: AIK and HAMAG-BICRO who are in charge of coordinating and checking that what is required is actually performed.